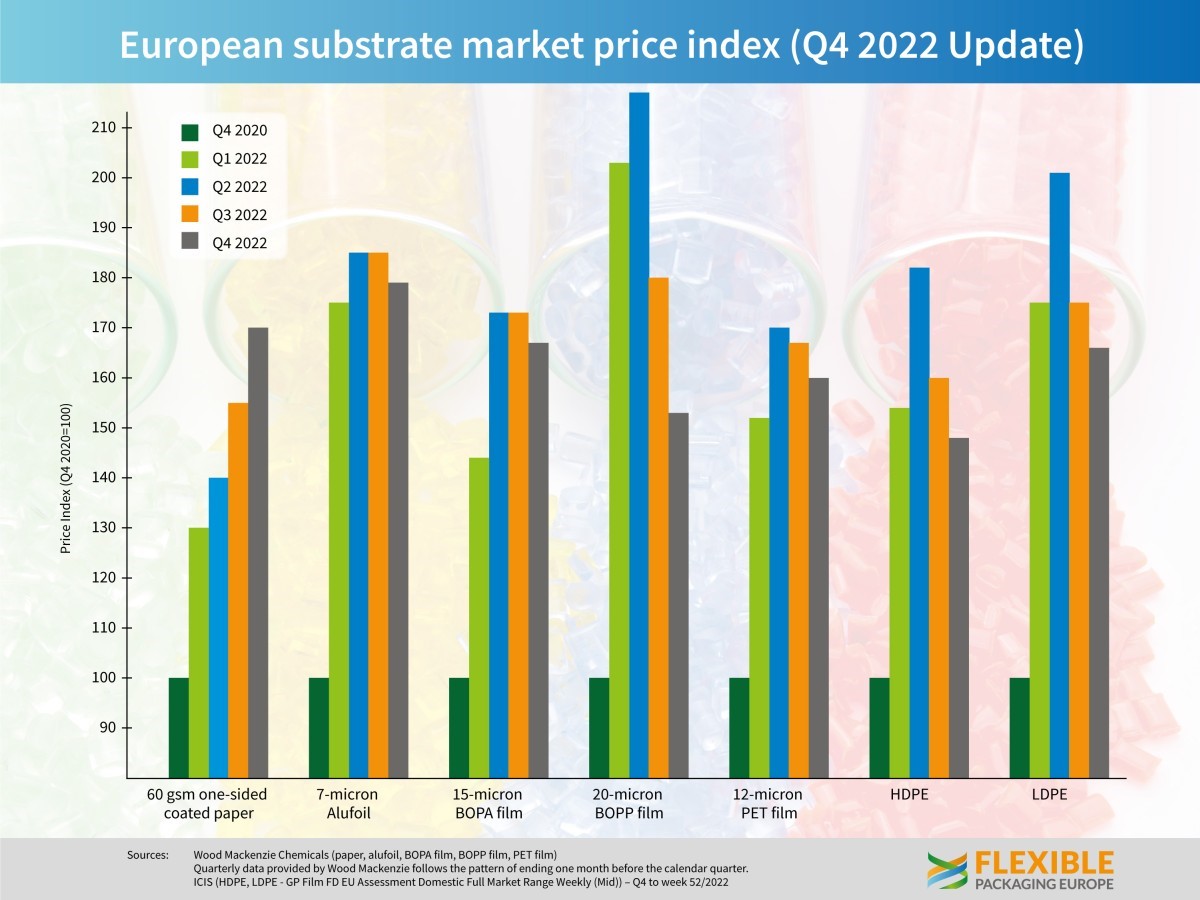

The last three months of 2022 saw declines in the price of some flexible packaging materials, as demand stabilised amid continued uncertainty about the global economic outlook and energy costs. After the peaks mid of 2022, most substrate prices registered single digit declines, according to figures released recently by Flexible Packaging Europe (FPE). Only 60gsm one-sided coated paper bucked the downward trend, as it did in Q3, as the price increased 10% from October to December, ending 2022 42% higher than the previous year. The only material to register a double digit decline was 20 micron BOPP film, down 15% on the preceding quarter. HDPE and LDPE fell 7 and 6 percent respectively, ending the year broadly the same as the end of 2021. Aluminium foil (7 micron) fell marginally by 3%, but still 21% ahead of December the year before. While both 12-micron PET (down 4%) and 15 micron BOPA (down 3%) films hover around 20% above their 2021 levels.

Assessing the latest figures David Buckby, senior analyst at Wood Mackenzie said, “Sluggish demand and high levels of uncertainty pushed most substrate costs down in Q4. Each stage of the value chain sought to run down their inventories, but this process is being lengthened by weak consumer demand. Several material suppliers and converters noted Q4 volumes being down by double-digits year-on-year.”

“Lower raw materials prices also supported substrate price reductions, as did excess global capacity in markets like BOPET film. Energy costs were a mixed bag. While some film suppliers absorbed hikes in Q4 others noted that prices had come down from the peaks seen in the summer but are still on an extremely high level. Lower container costs also supported reductions for offshore materials,” he added. “Flexible packaging papers were the exception, as prices increased in the quarter due to higher energy costs and previous increases in pulp costs having an impact.” FPE Executive Director Guido Aufdemkamp concludes, “The average price increase across all flexible packaging materials averaging more than +60% compared to one year ago are a burden for the entire supply chain. In particular during times of almost recession and high inflation this does not support extraordinary volume growth for the flexible packaging sector – although the resource efficiency of flexible packaging still provides absolute cost and environmental advantages compared to other packaging applications. The uncertainty over raw material supplies and supply chain disruptions due to the geopolitical situation continue.

{kind=link}