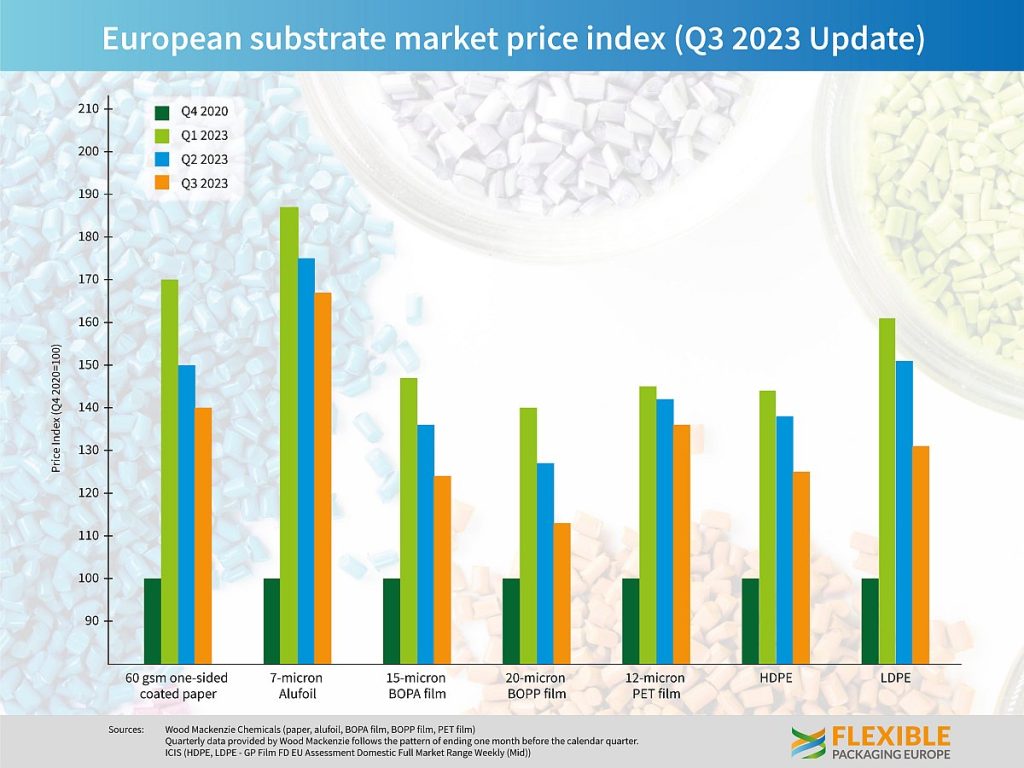

While there were gains in the price of HDPE, up 7% on the previous quarter and LDPE, up 8% in the same period, other results were patchier. The continuing weakness in demand and now the volatile situation in the Middle East, adding to the Ukraine war uncertainties, have had a negative impact on the outlook for 2024.

There was a modest decline in the price of 7-micron aluminium foil (4%) . Elsewhere 60gsm one-sided coated paper fell 7% against the Q3 figures while both BOPP 20-micron film and 12-micron PET film remained unchanged. A modest rise of 1% for 15-micron BOPA film completes the end of year figures.

While prices continue to drop or stabilize most are still well above the benchmark price from Q4 2020. 60gsm one sided coated paper, 15-mircon BOPA film, 12-micron PET film, HDPE and LDPE generally remain between 30-40% above that benchmark, and aluminium foil remains 60% higher. Only 20-micron BOPP film is returning towards the 2020 measure, at 13% above that price. However, all these prices are well off the peaks seen in mid-2022.

“Prices paid in Europe for flexible packaging materials were uneven in Q4. They decreased for both alufoil and one-side coated paper. Alufoil price declines were mainly due to conversion cost reductions. Paper pricing tended to be stable for small and medium-size customers, while some large buyers agreed reductions,” according to Santiago Castro, Senior Research Analyst, Films and Flexible Packaging at Wood Mackenzie.

“For BOPET and BOPP, prices remained stable on average. With demand flat, some attempts by suppliers to increase prices were rebuffed. BOPA prices rose marginally in Q4, driven mainly by increases in the price of PA6 resin,” he continued. “As for Q1 2024, consumer demand is expected to remain subdued. Inventory rebalancing has mostly ended. The situation in the Red Sea is putting pressure on imported raw materials, which could well drive prices up.”

Adding his views about the latest figures Guido Aufdenkamp, Executive Director of FPE commented, “The combination of very high stocks along the supply chain and pressure on end-consumer demand due to high inflation was not favourable for flexible packaging manufacturers and caused a decline of deliveries in 2023. There is continuous uncertainty due to the various conflicts in and around Europe and throughout the world bring, but recovery of the European economy, dropping inflation in most regions and stabilisation of retail sales volumes should have a positive overall influence. The industry is cautious optimistic for 2024 when comparing the demand of flexible packaging with last year.”

{kind=link}